Content

Items such as payroll expense may be earned by employees during the last weeks of the year, but not paid until after year end. In this way, expenses incurred in one year are properly matched with revenues from the same period. As far as tax payments go, there is a major benefit to switching to cash accounting. By eliminating accounts receivable, your income immediately lowers. Something very favorable to small businesses that don’t need to follow accrual accounting.

Is accrued revenue a debit or credit?

When accrued revenue is first recorded, the amount is recognized on the income statement through a credit to revenue. An associated accrued revenue account on the company's balance sheet is debited by the same amount in the form of accounts receivable.

Accrual accounting records revenue and expenses when transactions occur but before money is received or dispensed. When you fill out Form 3115, you report the section 481 adjustment. The 481 adjustment corrects issues with duplicating or omitting transactions during the transition. The section 481 adjustment reflects the https://www.bookstime.com/ changes you made to your books when switching from cash basis to accrual. As your business grows, you might consider switching to the accrual accounting method. Accrual accounting offers several perks for financial management. And if your business grows to a certain size, you might be required to use accrual accounting.

How to Figure Out What Is Going to Be Understated or Overstated in Accounting

An accounting or tax professional can provide additional advice on the conversion process and how this change affects a company’s financial statements. Some farms may choose to report income and expenses for tax purposes using accrual accounting methods. In that case, the gross income value shown on line 50 of Schedule F can be entered on line 1 of the worksheet.

- It also redefined a small business as “a corporation or partnership with less than $25 million in gross receipts for the prior three-year period”.

- Regardless of what basis you use to run your business or report your taxes, it’s helpful to analyze your company’s performance from different angles.

- Machinery, equipment, buildings and land are occasionally sold, and are recognized in the year when the sales are made.

- Then make all the necessary subtractions and additions to get the right figures for your taxes.

- It is always good to be cognizant of tax changes, some could be beneficial to your business.

Accrual-basis recognizes revenues when earned and expenses when incurred even if cash has not been received or no cash has been paid. Furthermore, it is also important to consider the fact that several different heads of accounts are included in the accrual basis of accounting, not the cash basis of accounting. If the company receives an electric bill for $1,700, under the cash method, the amount is not recorded until the company actually pays the bill. However, under the accrual method, the $1,700 is recorded as an expense the day the company receives the bill.

Central Service Provider Accruals

Revenue is recorded even if the cash has not yet been received. The more complex accrual method requires a greater understanding of accounting principles, but reported results are more accurate. We incurred the expense in the prior period, meaning we already recorded it. Once it is paid we reverse the entry, but it does not belong in the current period.

How to Prepare Adjusting Entries: Step-By-Step (2022) – The Motley Fool

How to Prepare Adjusting Entries: Step-By-Step ( .

Posted: Wed, 18 May 2022 07:00:00 GMT [source]

Rather these are charged to a special Controller’s office department. These accruals are generally determined after the general ledger is deemed final for Information Warehouse reporting. Breeding livestock raised but not sold during the year are accrual-adjusted to the current year. Production from these animals contributes to income; however, their change in value also affects income. The IRS does not allow the cost of feeder livestock or other assets purchased for the purpose of eventual resale to be deducted until the tax year in which they are sold.

How to Find Net Income From Unadjusted Trial Balance

For every business transaction, you record at least two opposite and equal entries. Debits and credits increase or decrease the accounts in your books, depending on the account. In this article we will discuss about the conversion of accrual basis income to cash basis income. To illustrate, let’s assume your business received an electric bill for the month of July, and its due date is on August 10. Under the accrual method, you need to recognize the utility expense in July because the electricity consumption is for the month of July. Hence, accrual records must debit utilities expense and credit utilities payable.

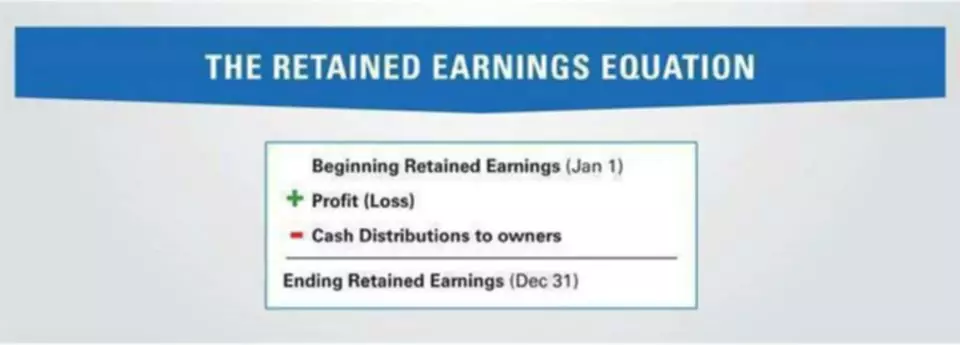

Select “display” tab and click “cash” or “accrual” in the report basis section. The conversion for the second year gets a little more complicated. If we just reverse the current year receivables and payables then the beginning retained earnings will be off by $5,000. This video accrual to cash adjustment illustrates potential impacts on farm businesses due to the newest rules from the US Dept of Labor. We realize though that we want to have a more precise account of the values produced during this year, and that’s why we need to adjust this adjustment to accrual-basis.

How are Financial Statements Different in Accrual Accounting?

For accrual accounting, record the prepayment as a short-term liability until you provide the good or service. To convert to accrual, subtract cash payments that pertain to the last accounting period. By moving these cash payments to the previous period, you reduce the current period’s beginning retained earnings. When you convert to accrual accounting, move any prepaid expenses from the current accounting period to an asset account. Prepaid expenses are cash payments you made that relate to assets you haven’t used up yet. You pay for something in one accounting period but don’t use it right away.

- Reflects profitability of a typical year for the farm business.

- For example, a business could decide to pay off all their expenses at the end of their tax year to lower their tax bill even if those expenses weren’t due at the time.

- Pumpkins are well-suited to small-scale and part-time farming operations.

- Hence, accrual records must debit utilities expense and credit utilities payable.

- We incurred the expense in the prior period, meaning we already recorded it.

When the company pays the invoice, we will always debit accounts payable to remove the liability and the offsetting credit will be to cash for the cash outflow). A company will likely receive an invoice for any product or service purchased from a 3rd party / unaffiliated company. Do not include expenses for any accounts payable that were not actually paid in cash during the period. For example let’s say year end A/R for 2018 is $20,000 and for 2019 is $28,000.

Cash Basis Method of Accounting

While making conversion, one should know the relationship between income statement accounts and balance sheet changes. Each individual item on the income statement should be viewed as it relates to a balance sheet account. Cash vs accrual accounting isn’t an argument of which method is better. Rather, it’s a business decision grounded on how the information will be used and the difficulty in producing accrual-basis financial statements. Many businesses will use the cash-basis for income tax returns and the accrual-basis for financial reporting. However, some very small businesses will produce cash-basis financials because accrual-basis accounting is too complex and difficult to apply.

- She holds an MBA from the University of Illinois at Springfield.

- However, the cash basis method might overstate the health of a company that is cash-rich.

- For example let’s say year end A/R for 2018 is $20,000 and for 2019 is $28,000.

- A chart of accounts is a map of all financial accounts in the general ledger.

- For example, if you prefer a tax deduction in the current year, the expense can be paid at the end of December.

- Some accountants prefer to leave Client Deposits and/or Vendor Deposits on the balance sheet.

- The increase in the gross receipts threshold from $10 million to $25 million creates an opportunity for more contractors to take advantage of the cash method.